Making A Positive Transition To Retirement

Most people spend decades planning the financial side of retirement and almost no time planning what they’ll actually do with it. Then the day arrives, the alarm clock goes silent, and the question lands: now what?

Retirement is one of the biggest identity shifts you’ll ever go through. For thirty or forty years, a large part of who you are has been bound up in what you do. When that goes, even people who couldn’t wait to leave can feel oddly unmoored. The good news is that the people who settle in well tend to have one thing in common: they treated the non-financial side of retirement as something to plan for, not just drift into.

Transitioning to retirement may be a bigger change than you expect

Work gives you more than income. It gives you structure, status, a built-in social circle, and a reason to get up. Lose all of that in a single week and the freedom can feel less like a holiday and more like a void.

This is worth naming because the people who struggle most are often the ones who assumed they wouldn’t. The advice to “relax and enjoy it” sets you up to feel like something’s wrong when relaxing turns out not to be enough. It usually isn’t. What replaces the structure of work is the real project of the early years of retirement, and it’s worth thinking about before you stop, not three months after.

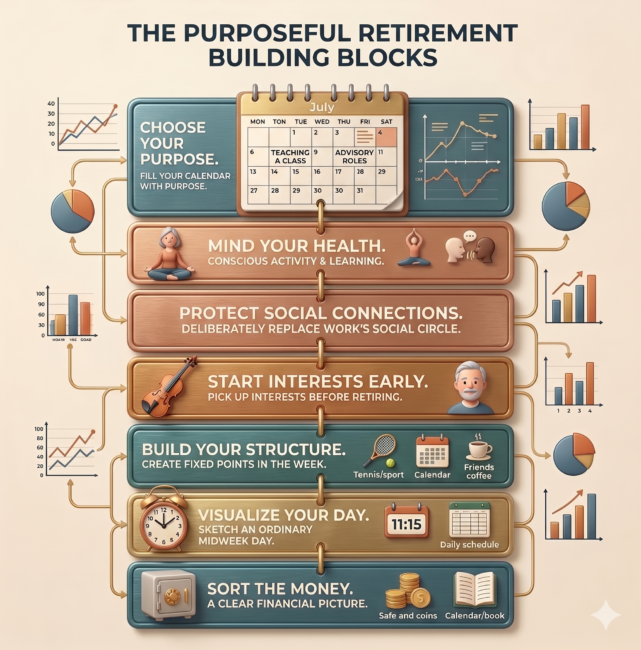

Sort the money so it stops being a worry

You can’t enjoy your time if you’re quietly anxious about whether it’ll last. Before the lifestyle planning means much, the financial picture needs to be clear enough that you’re not second-guessing every spending decision.

That means knowing three things with reasonable confidence: what your income will actually be once you stop earning, what your spending genuinely looks like (not the rough guess most people carry in their heads), and what happens if something goes wrong. A sustained market fall in your first few years, a care need later on, the loss of one partner’s pension income; these aren’t pleasant to model, but modelling them is what turns a vague sense of “we should be fine” into something you can stop worrying about.

A realistic budget is messier than the textbook version. Spending in retirement isn’t flat. Many people spend more in the early, active years, less in the middle, and then more again later if care comes into the picture. Building a plan around a single average figure tends to hide that. This is the part where getting proper advice earns its keep, because the decisions around drawdown, tax, and sequencing are genuinely hard to get right alone, and the cost of getting them wrong compounds quietly over decades.

Build the structure before you need it

Here’s a practical exercise. Sketch out what a normal Tuesday looks like in your retirement. Not a holiday, not a special occasion, an ordinary midweek day. People who can answer that in detail tend to do well. People who can only describe holidays and Christmas often find the ordinary weeks harder than they expected.

The aim isn’t to fill every hour. It’s to have a few fixed points in the week that you’d miss if they vanished: a regular tennis morning, a volunteering commitment, a standing coffee with friends, a course with a term that runs to a timetable. Commitments with other people attached are the ones that stick, because they don’t quietly evaporate the way solo good intentions do.

It also helps to start before you finish work. Picking up an interest while you still have the routine of a job makes it far more likely to survive the transition. Waiting until day one of retirement to invent a whole new life from scratch is a lot to ask of yourself.

Protect the social side deliberately

This is the part people underestimate most. A surprising amount of adult friendship is logistical. It runs on shared context and proximity, and work quietly supplies both. Remove it and the friendships built around it can thin out faster than you’d think, often without anyone deciding anything.

So the social side needs replacing on purpose. That can mean keeping in touch with former colleagues, but it’s usually healthier to build connections that don’t depend on a job you’ve left. Clubs, classes, volunteering, a sports team, a regular group of any kind; the specific activity matters less than the fact that it puts you among the same people often enough for actual friendships to form. If you have a partner, this matters for you both individually, not just as a couple. Two people retiring into each other’s full-time company, with no separate outlets, is a common source of friction.

Mind the obvious health stuff

You don’t need a lecture here, but two things are worth saying plainly. Physical activity does more for mood, sleep, and sharpness than almost anything else available to you, and retirement removes the incidental movement that work used to force on you, the commute, the walk to a meeting, the stairs. That has to be replaced consciously.

And mental engagement matters in the same way. The brain holds up better when it’s regularly asked to do something genuinely unfamiliar, which is different from comfortably repeating things you already know. Learning a language, taking up an instrument, or anything with a real learning curve does more than crosswords you can already finish.

A more honest summary

A good retirement is rarely the one where you finally get to do nothing. It’s the one where you’ve replaced what work gave you, structure, people, purpose, progress, with things you actually chose. The freedom is real, but freedom on its own is just an empty calendar. The satisfying part is what you decide to put in it.

If you do the work beforehand, get the finances clear, build a couple of fixed points into the week, protect your friendships on purpose, keep moving, then retirement stops being a cliff edge and becomes what it should be: the part of life where your time is finally your own, and you’ve actually got a plan for it.

This is financial education, not regulated advice. Your own circumstances will differ, and decisions about pensions, drawdown, and investments should be based on advice specific to you.

Written by Jamie Kyte, a fully qualified, FCA-regulated Independent Financial Adviser at Kyte Financial Planning (www.kytefp.co.uk) based in London.

Newsletter Sign-Up

Looking For Retirement Advice?

Complete our short questionnaire and you’ll be put in touch with a Chartered Financial Planner who will discuss your personal situation with you.

Take a FREE Retirement Quiz...

It’s time to see if you’re on track with your goals, and what changes (if any) need to be made.